There's no point in credit card points: Cash back is the only way

Take five minutes and switch to cash back today—Your savings and the planet will thank you.

Two weeks ago, I was at the star-studded Elevate Tech Fest in Toronto. My favorite talk was with Michael Katchen, the Co-founder and CEO of Wealthsimple (see photo below). Most of my calculations assume investing your savings and there’s no better way to invest your money than in low-cost ETFs with a product like Wealthsimple. If you don’t already have an account, then this is a very important step to ensuring that your savings are growing. You can and should choose a socially responsible investment portfolio, both for the planet and for improved savings (there will be another post on this one day).

Choosing From a Sea of Credit Cards

In this post, I’m going to show you how choosing the right credit card, something that will take you five minutes and zero upfront investment, will protect the environment, provide you with more control over your life, and of course make you wealthier.

Warning: If you do not think you’ll be able pay off your credit card in full every month, do not get any credit card, no matter what. There is no rewards program that merits the interest rate that you’ll be charged for carrying a balance, even one month per year.

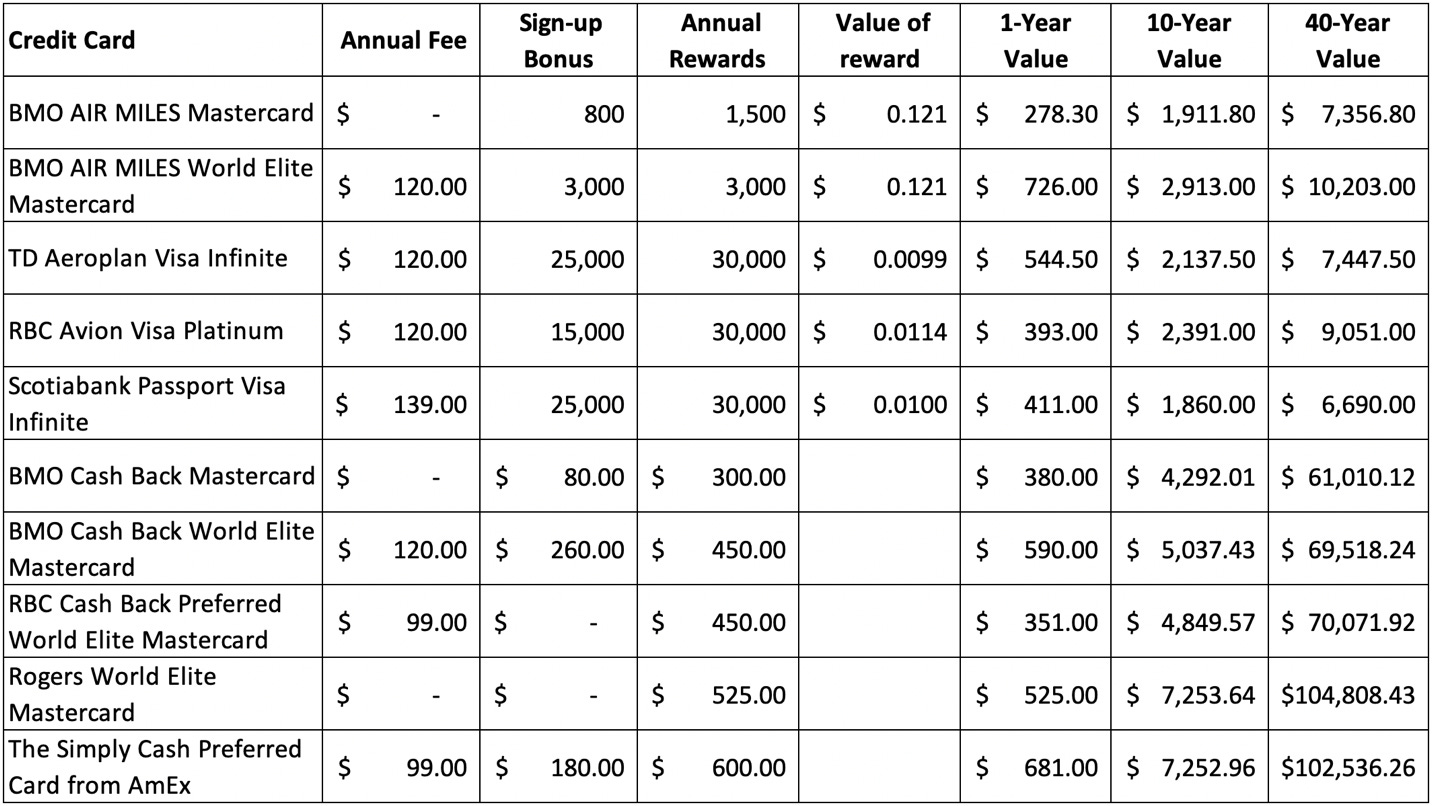

I’ve completed the exercise of comparing ten very different Canadian credit cards. Some that give you air travel points, some that have their own rewards programs and others with cash back. I took into account any sign up incentives, whether there were points, cash, discounts, bonus rates or any combination thereof, chose a mix of expensive “high-end” cards and free cards, and found evidence for the dollar value of each type of points program when exercised. The value of each type of points was determined for Scotia Rewards, Air Miles and Aeroplan from RateHub, and Avion here. If you think I have missed a card that is much better, I encourage you to leave a comment and I will add it to the analysis if it makes sense—let’s get the conversation going! That being said, the exercise was to compare rewards programs with cash back cards and the results speak for themselves. Trust me, your points card is not the exception to the rule, but, if you think it is, I will be happy to add it to the analysis.

Table 1: Comparison of 10 different credit cards for someone that spends $2,500/month on average and invests their savings.

Note: All cards have additional bonuses like extra points on gas or groceries or a better cash back rate on certain bills. Let’s assume that the additional bonus rates don’t affect your rewards materially and that all cards have comparable bonus rewards. It’s also worth noting that these offerings often tie you down to certain partners (i.e. “twice the points at participating retailers”), which is terrible for your consumer choice. In summary, we should not be choosing cards based on these bonus rewards.

How Much Will You Save With Cash Back?

Looking at the table above it’s clear that for someone who spends $2,500/month on their credit card, the best cash back card will generate an extra $4,340 of savings over ten years and $94,605 over forty years more than the best points card does in equivalent points value. For a middle-class Canadian family that spends $6,000/month on two family credit cards, the ten- and forty-year differences in savings by choosing cash back balloons to $11,300 and $241,000, respectively. If this doesn’t compel you to ditch your points card for cash back then I don’t know what will, but I’ll do a deeper comparison of the best points card versus the best cash back card just to illuminate this difference even further.

Points vs Cash Deep Dive

If you’re using a points card, then you are almost certainly going to spend the points on flights. Of course, all the points programs allow you to spend them on a new TV or toaster oven, but the best value for your points is clearly to spend them on flights. Using your points for anything else is just burning money and limiting your consumer choice to the things that they’ve put in front of you.

In this comparison, I want to show you that even though you’re getting lots of flights with your rewards, you would be able to buy all those flights and more with your cash back. I will give points users the benefit of the doubt in picking great flights and booking long in advance, even though it’s rare for people to get the minimum posted rate and the flight they actually want. Over ten years, someone spending $2,500/month with their BMO Air Miles World Elite Mastercard (best points card in Table 1) will:

get 33,000 Air Miles,

convert them into anywhere from 7 to 16 flights in North America,

fork out an additional $129 to $163 in taxes and fees on each flight,

and create a hole in their savings of somewhere between -$1,148 and -$2064.

The same person with a Rogers World Elite Mastercard can decide to fly less and save a lot more money, or fly the same amount as the points user, buying all those flights with cash, and still end up with between $3,313 and $4,086 in their savings account! Of course, this difference balloons over 40 years.

Which Cash Back Card is Best for You?

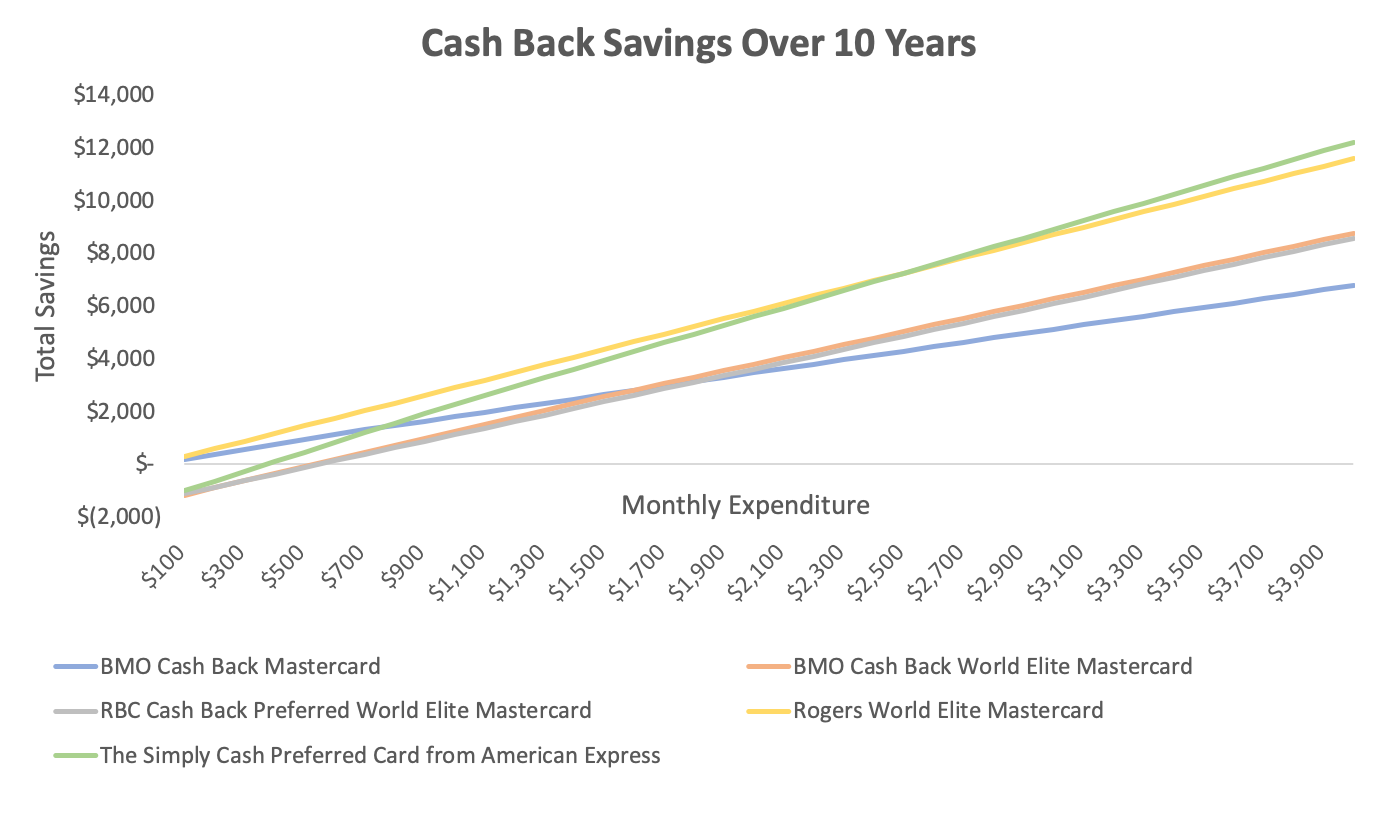

Now that you can see that points cards are terrible and cash back cards are the only way to go, let me help you pick which cash back card is right for you. In the chart below you will see the total savings over ten years for five cash back cards at various levels of monthly expenditure on your credit card. If you’re spending on average about $2500/month or less on your credit card then you should get the Rogers World Elite Mastercard (note: there is a high income requirement) and if you’re spending more than that, then you should be getting the Simply Cash Preferred Card from American Express. That being said, I’ve done some research on American Express and it’s not accepted everywhere, especially in Canada, so the Rogers World Elite Mastercard might be the best card for some.

If you would prefer to just choose from the credit cards at your bank so that everything is in one online banking dashboard, I get that, but you’ll be forfeiting some savings for convenience. In that case, the cash back cards from the big banks are pretty much the exact same, so you can use the two BMO cards on the above chart as a proxy. If you’re spending more than about $1600/month on average, then it’s worth upgrading to the card with more cash back even though there’s an annual fee.

Not everyone will meet the income qualification required for the Rogers card, but the most important thing is that you’re using a cash back card. Even the free, and no restriction, BMO Cash Back Mastercard is much better than it’s points-based counterpart.

How Does Choosing the Right Credit Card Help the Environment?

From an environmental perspective, if everyone switches to cash back then there will hopefully be less flying. If you are going to fly the same amount with a cash back card, then your environmental footprint will be the same as with a points card and you’ll have some extra money to spend while on vacation. However, you may decide that, this year instead of flying, you’ll put that money toward a down payment on an electric car and go on a road trip instead. Or you’ll visit your parents via the train and have a more pleasant experience instead of always flying. If all you have is air miles then of course you’re going to always be flying, but if you have the option to spend your money elsewhere then you’ll likely have a smaller environmental footprint and a larger bank account.

For those that fly a couple times per year or more, flying is one of the largest contributors to their carbon footprint. A five-hour round-trip economy flight from Toronto to Vancouver spews 1.07 tons of CO2e into the atmosphere, the same amount an average Canadian emits driving a gasoline vehicle every day for two or three months.

Don’t Live in Canada?

I know I have only compared Canadian credit cards in this article, but the principles are the same no matter where you live. The most important thing is that you never carry a balance and always choose a cash back card. Once you have this covered, you’re 90% of the way there to maximizing your savings. I’m sure the cards in your country will line up pretty closely with what I’ve compared here, but if they don’t, please comment on this post and I’d be happy to look at a few other countries as well.

If you found this interesting or helpful please subscribe to the newsletter and share it with someone who collects points.