An Emergency Reminder

Take a deep breath and bring it back to the basics

Take Pause, and Reflect

In March, when almost overnight the pandemic forced the world shut down and the stock market had the sharpest crash in history, I wrote an article asking everyone to keep their hands clean of stock market panic and stay the course. If you had not touched your investments and continued to invest throughout the pandemic, you were handsomely rewarded. Though, I would have never guessed in a million years that, still in the throes of the pandemic, we would be at new all-time stock market highs with the largest indices up 40-70% in only seven months.

We must count our lucky stars and then take a moment to evaluate our finances, be financially prudent, and ensure our portfolio is properly diversified. After seven months of huge gains, it can feel like the stock market can only march higher. It may or may not, nobody can know for sure. However, today’s short post is a reminder of one very important investment principle…

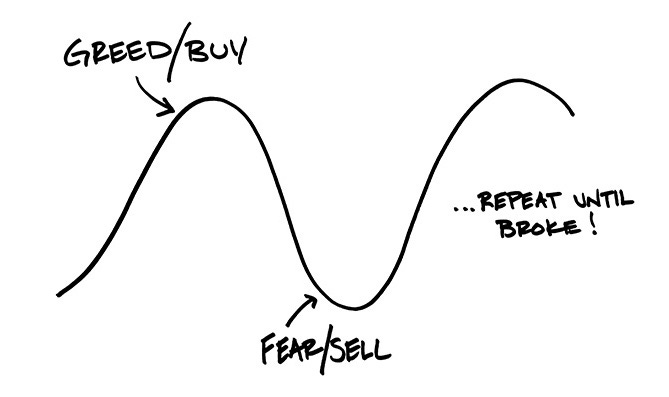

If the market were to start free-falling again because of the US election, further catastrophic climate events, a larger second wave of Covid-19 than expected, or for any one of a million reasons, the economy could be in a much worse place this time and for a much longer period of time. In times of economic pain, people are more likely to lose their income and have unforeseen expenses. In this situation, the worst possible thing for your long-term finances is if you’re forced to sell your hard-earned investments at the bottom.

Instead of buying high and selling low, we want to buy low and sell high (or never sell). How can we avoid this fate if something terrible and out of our control happens?

An Emergency Fund

One of the core tenets of personal finance is that everyone should have an emergency fund. An emergency fund should eventually be about six to twelve months worth of living expenses in cash or cash equivalents that you can rely on in a tough time, without having to sell off your long-term investments.

In order to determine how much savings should be in your emergency fund, just take your monthly expenses like rent, your car payment, credit card bill, utilities, etc. and multiply it by six to twelve.

If you think your job is recession proof, like a healthcare worker or tradesperson, you can lean towards six months but if you’re in a more boom and bust industry like tech, energy, or retail you may want to lean towards twelve months. If you don’t have enough savings to cover six to twelve months of living expenses, that’s ok, but it’s time to start saving.

To be clear, in no way am saying that I think the market is going to crash and that you should sell everything. I do not know that, and I’m absolutely not saying that. If the stock market continues to go up for the next ten years, by having an emergency fund you’ll miss out on a bit of stock market gains, but if the market crashes, you lose your job, and you’re forced to sell all your investments to cover your living expenses, all of your investments could be lost. Now is the time to build your emergency fund.

“The best time to plant a tree was 20 years ago. The second best time is now.”

Why am I bringing this up now? Well, it’s always important, but after the big run-up that we’ve seen in the stock market, if you don’t have an emergency fund but own a lot of stocks or ETFs, you’re at risk. I’ve seen a lot of people getting overzealous about the stock market, there’s more new stock market investors than ever before, and maybe, just maybe, some of us have gone too far and forgotten our principles of diversification. This is a great opportunity to take some gains and protect yourself against a possible reversal with an emergency fund.

If you missed out on the massive run-up in the stock market and don’t have any investments, don’t worry, it’s never too late to get started. If you feel like six to twelve months of living expenses is impossible for you, that’s ok too, start with one or two months and contribute to this fund every month. Now’s the time to start building up your emergency fund and once you have that, you can start dipping your toes into some more risky, long-term investments.

Sustainable Savings

I don’t have anything to say about sustainability in this article, however, if you’re looking for ways to reduce your monthly expenses so that you can build your emergency fund, I’ve written many other articles about how to build wealth while protecting the planet.

Thanks for reading The Lean House Effect.

If you’re diggin’ TLHE, please consider doing two quick things:

1) Forward this email to a curious friend (they can signup here). 🙏

2) Consider subscribing for premium content and I’ll have two trees planted on your behalf every month. 🌲 🌲

Till next month,

Jacob

P.S. some quick “lean” housekeeping—Gmail users, these emails will eventually default to your “Promotions” tab (lame), so be sure to add “green@substack.com” to your contact list, or simply drag the newsletter from your Promotions inbox into your Primary inbox.